When Inflation is the Best Outcome

In May of this year, a ratings agency downgraded the sovereign credit of the United States.

A few days later, a Treasury auction of 20-year bonds met with an unexpectedly chilly reception. Sudden anxiety permeated the upper echelons of the Administration, followed by loud demands for Jerome Powell to reduce interest rates, then the floating of some far-out schemes for selling bonds, or somehow extracting money from the Fed.

Why the panic?

It might seem an episode only a banker could care about. But understand the hidden magnitude of US borrowing, and it begins to make sense. Yes, we have a big annual deficit, now on the order of 6% of GDP, and growing. And the Treasury has to fund this by borrowing money. But it’s the tip of the iceberg.

What lies beneath

Every year about 20% of the government’s debt matures and has to be repaid. Since our government does not collect enough revenue to balance the budget, this is also funded by borrowing (sometimes referred to as “rolling over” debt). The total US debt now stands at 120% of GDP (1.2 times our total economic output), so new bonds worth 24% of GDP must be issued each year just to repay what comes due.

Between this and funding the deficit, the Treasury is now borrowing at the rate of 30% of GDP, every year. And even though most of this new debt is exchanged for old, it means that the annual interest bill added to the rest of public spending can ratchet up very quickly.

And it did.

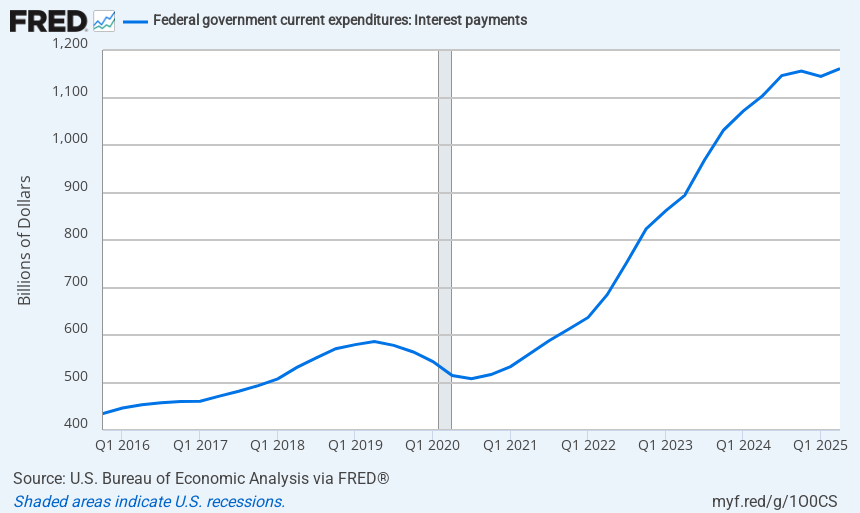

From a low of around $500 billion at the depths of the pandemic, the annual interest bill has surged to well over $1 trillion – which puts it ahead of the defense budget – due to a combination of deficits and spiking interest rates. So you can understand the President’s desperation in demanding Jay Powell bring down rates, but you should also understand why it won’t help.

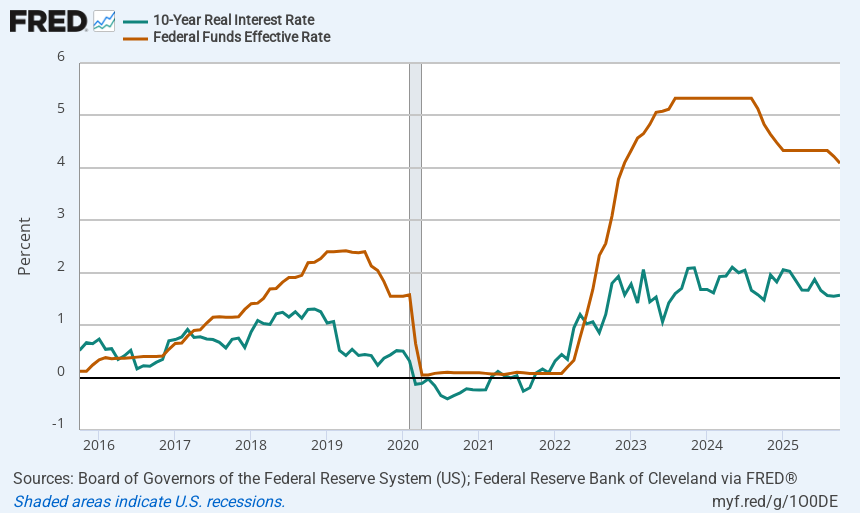

Unfortunately, the easiest way to show this is with another chart.

The red line represents short-term rates, which the Fed controls, while the blue line is a long-term inflation-adjusted rate (which, after adding back inflation, is what the Treasury pays on its 10-year bonds). You can see where the Fed jacked up rates to choke off inflation, beginning in 2022, and where it began cutting again in ’24 and ’25. But what should jump out at you is this: long term rates did not follow the Fed down. They remain elevated.

You see, no one can tell the market at what rate to loan the government money. Bonds are sold at auction, and if the market doesn’t like the rate marked on the bond (electronically, of course), they’ll simply bid down what they’re willing to pay. If the Treasury auctions a $50,000 bond (face value) marked at 4% interest, they may only be able to sell it for $45,000. But they still have to pay the full interest of 4% on $50,000, or $2,000/yr. So the new bond owner gets 4.4% interest on his $45,000 loan, and oh by the way the full sum of $50,000 when the bond matures.

This is what we mean by “bond vigilantes”. The market is the market. And people loaning money for 5, 10, 20 years, or more, and for single-digit interest, are very sensitive to losing money – say to inflation, while waiting for their bonds to mature, or to a loss, if they have to sell their bonds at a time when rates are up, again due to inflation or maybe a financial crisis. And these are real concerns.

Have we got a deal for you

Secretary Bessent is probably well aware that the President’s public haranguing of Powell can only make matters worse. But he has an idea.

You may remember that something called the GENIUS Act became law in July of this year. It provides a regulatory framework for a type of cryptocurrency called stablecoins. Stablecoins are backed by very safe assets, meaning treasuries. Hence their value should be tied to the dollar, and their issuers should always be able to redeem them, on demand and at full value.

Bessent’s idea is that new issuers of stablecoins will enter the market for treasuries, helping to bid up the prices and hold down the effective rate of interest.

Clever, eh?

Well, you might remember Silicon Valley Bank, even though SVB is no longer with us. It failed in 2023. This happened after a run on its deposits, which came about when the general rise in interest rates (fighting inflation) caused its reserves of securities, like treasuries and mortgage-backed securities, to lose market value just when the bank faced escalating withdrawals, meaning escalating demands for cash. Big depositors, worried about SVB’s deteriorating balance sheet, accelerated their withdrawals – to avoid the very bank run they ended up causing.

But that’s how runs work. What looms as a potential disaster should everyone head for the exit at once, becomes an actual one, as everyone heads for the exit to avoid it.

The thing to remember is that stablecoin issuers will be in business to make money. They will compete to get “deposits”, which they will use to buy securities like treasuries that pay interest, and they will collect that interest to fund their expenses and profits. And whatever regulations put in place today will be loosened over time, and under intense lobbying pressure, as the industry seeks to fatten its profits. (See the S&L crisis.)

So, yes, stablecoins might help trim the interest paid by the US on its debt, but only marginally, and the idea of trillions of dollars siphoned into an industry very closely resembling deposit banking, but capitalized almost entirely with treasuries, should be unnerving – as is the idea that this is the best solution anyone can come up with.

Didn’t we fix this once?

When you think about how much money you owe, to be sensible about it you also have to think about how much you bring in. $10,000 in credit card debt is manageable if you make $100,000 a year and don’t owe anything else. It’s catastrophic if you make $20,000.

So the best way to think about the national debt is not the absolute number, but in relation to the national economy.

- Shortly after the end of the Second World War, the national debt had reached nearly 120% of GDP, the result of a long, very expensive war of attrition. At that time, this was universally regarded as unsustainable.

- Under the stewardship of five presidents, from Truman through Jimmy Carter, the ratio dropped, decade by decade, to 30%.

- Under Reagan, everything changed. By the time he left office, the debt had ballooned to over 50% of GDP, then to over 60% when his successor, George H. W. Bush, finally stepped down.

Then along came a new guy.

Even before he was sworn in for his first term, Bill Clinton and his transition team found that the deficits they were inheriting from the Reagan era were going to be much higher than had been imagined. So they scrapped their spending plans and went to work rethinking the budget.

In February, 1993, the new administration submitted their proposal to Congress, a five year plan that combined small tax increases with selective spending cuts. Defense would be trimmed, and there would be a cap on how much Medicare spending could rise. A freeze would be imposed on other discretionary spending.

The tax on top incomes would be raised to 39.6%, from 31%. The top corporate tax would be raised to 38%, from 34%. Other minor tax increases were listed, including a reduction in the deductibility of business meals, as well as scrapping deductions for club dues – which was probably rubbing salt in the wound.

Conservatives exploded, savagely attacking the plan and the administration. According to Senator Pete Domenici, top Republican on the Budget Committee, the tax increases would “devastate the economy”. Senator Phil Gramm, who liked to pose as a steely-eyed budget expert steeped in serious economics, held a press conference on the steps of the capitol to declare that the plan would lead to a recession, or even a depression.

In the House, every Republican voted against it. It passed.

The Senate deadlocked, 50-50, until Vice President Gore cast the deciding vote to break the tie.

In 2016, Bloomberg published something of a retrospective, with excerpts from interviews with some key figures.

George Mitchell, Senate majority leader: Every single … Republican voted against it and almost all of them said that if Clinton’s budget passed, interest rates would go up, unemployment would go up, the economy would tank, job creation would go down, inflation would rise. In other words, what they said is all the bad things would go up and all the good things would go down. And of course as we all know, the opposite happened. All the good things went up, and all the bad things went down. They were 100 percent wrong.

Roger Altman: One of the many stunning things about [that vote] is the fact that none of those Republicans paid a price of any kind for that… [Senator] Phil Gramm (R-TX), I’ll never forget, predicted that it would usher in a new depression — I mean depression, not recession. He voted against it; we had a boom — he never paid a dime’s worth of price for that.

Alice Rivlin: I think there were multiple causes for the boom of the 1990s. … By the mid-1990s we were able to take advantage of the potential of information technology for increasing productivity, and the economy just took off. The increase in the rate of productivity increases is what is really significant here.

But I think policy helped…. We finally got the budget deficit coming down and very low interest rates…

So it all came together in the ’90s: the technology, the good policy, the readiness of American industry to take advantage of it…

For One U.S. President, Deficits Mattered, Bloomberg, September 1, 2016

Level-headed people clearly understood that Clinton and his team did not cause the economic boom, but they also understood that the new fiscal discipline was a key factor, and especially in the decline of interest rates. Not only did the deficit go down, allowing the economy to grow faster than the debt, but for a while the budget actually went into surplus.

The Left and Right agree on something

Clinton’s administration was decidedly centrist, much to the disgust of both progressive Liberals and the hard Right. “Deficits don’t matter” was the mantra of Bush/Cheney going into the 21st century, echoed later by Progressives who discovered something called “Modern Monetary Theory”. The Right claimed that the magic potion of tax cuts would create so much growth that the fiscal mess would take care of itself, while the Left shrugged, “What mess?”

The Right blames every financial crisis on government regulation, while the Left blames greed, but in the end they both join hands to dig the hole deeper.

Does it matter? The episode last May was a warning that it will. The sovereign financial credibility of the United States has been declining for years, with three credit downgrades since 2011, and repeated Congressional showdowns over the debt ceiling – which is becoming a dangerous form of political hostage-taking, as it potentially threatens default. Borrowing costs may go up and down from year to year, but a risky creditor who thinks his credit doesn’t matter will pay a lot more in the long run.

When you realize you’re digging a hole for yourself, the best advice is not to look for more places to hide the dirt.

But that, of course, is just what we’re doing, and will almost certainly continue to do. Bessent’s crypto scheme, like other schemes before it, may buy time, but as the hole continues to deepen, it will eventually become urgent to defuse the threat of default.

Default is the unthinkable. In one stroke it would destroy the country’s ability to borrow. Tens of trillions of dollars in treasuries would instantly crater in value, taking down a large part of the financial system and decimating the dollar. And for this reason you can expect it to become the ultimate political showdown.

With no political center, eventually the only course of action that Left and Right will be able to agree on, if tacitly, will be to inflate away the value of the debt. The hope will be that inflationary stimulus will inflate growth as well, allowing the value of outstanding debt to erode along with the value of money. They may also hope that the dollar will manage to remain the world’s reserve currency, if other Western democracies are forced pursue higher inflation as well, limiting the pain to a shared one.

That will be the hope. And it may be the best outcome that we can expect – where we all end up paying the bill over time, rather than all at once. And, of course, with no one to blame.

How do we move to the center and stop digging?

Wish I had an answer!